What SDVs Mean for the New Era of Automobiles: A Core Pillar of the Mobility DX Strategy Online Feature Updates Create Value Continuously

- # Interview with the METI

- # Mobility DX

Rising concern about the future of Japan’s cornerstone industry

In Japan—long exposed to the so-called “lost 30 years” and to an industrial shift centered on IT—automobiles have become an unshakable cornerstone industry. Recent economic statistics indicate that the sector accounts for roughly 20% of shipment value in domestic manufacturing, about 30% of capital investment and R&D investment, and 10% of domestic employment. Global competitiveness also remains high: in 2024, around 30% of worldwide vehicle sales were attributed to Japanese brands. With a broad base including parts makers and numerous regional hubs, it is an industry that underpins Japan’s economic strength.

However, the main axis of competitiveness is shifting—from areas where Japan has traditionally excelled, such as the reliability and safety of “run, turn, stop” and fuel efficiency—to the digital domain (DX). The driving force behind this shift is the emergence of SDVs. Fine-grained responses to user needs and enhancements to driving functions—in other words, the creation of new value—can now be realized through software updates on vehicles, without requiring time-consuming parts replacements. As highly competitive vehicles continue to be released, the conventional wisdom that “a car’s value is highest at the time of new-vehicle purchase” is beginning to be overturned. Makoto Kuroyabu, Director of METI’s Mobility DX Office in the Automobile Division, voiced a sense of urgency: “We have entered an era in which whether or not you can respond to SDVs creates a clear gap in competitiveness. It is not necessarily a safe future.”

Against this backdrop, METI and MLIT formulated the Mobility DX Strategy in 2024 as a roadmap for the automotive industry. With the goal of achieving a 30% global share for Japanese SDVs, it set out concrete measures including development of related technologies such as semiconductors and automated driving; data linkage among vehicle modules (functions); and the establishment of the Mobility DX Platform (PF), a community involving industries beyond automotive as well as startups and academia.

Yet in just one year after the strategy’s formulation, the environment surrounding SDVs changed dramatically. Competition in technology development intensified further as Tesla and Chinese manufacturers implemented E2E (end-to-end) approaches in which AI largely handles automated-driving control. Risks related to parts supply networks (supply chains) became clearer, and SDVs began to be discussed in the context of economic security as well. For example, a U.S. connected-car regulation that bans the import and sale of vehicles equipped with Chinese- and Russian-made components or software took effect in March 2025. Moreover, because communications are essential for SDVs—particularly for software updates—thorough cybersecurity is indispensable to ensure safety and security.

As challenges surfaced in quick succession, METI and others revised the DX strategy as early as June 2025. The key points were: (1) development and demonstration of E2E automated-driving technology; (2) building an industrial structure suited to SDV development; and (3) strengthening SDV-related supply chains to address geopolitical risks such as U.S. regulations. Kuroyabu said, “What matters is not the fact that we updated the strategy itself, but whether both government and industry can actually strengthen initiatives and deliver results.”

Rising concern about the future of Japan’s cornerstone industry

Put simply, the government’s SDV definition emphasizes vehicles that, in addition to information and entertainment (infotainment), are equipped with over-the-air (OTA) communications that enable updates to control software—centered on automated driving—for “run, turn, stop.” The image is that, like a PC operating system or game apps, online updates that expand functions and content will be applied to automobiles as well. Examples include improved compatibility with charging stations, optimized air conditioning, integration with entertainment apps, and two-way communication tools. Because SDVs can flexibly respond to needs that differ by individual user and by region, a rapid global market expansion is expected, including in Europe, the U.S., and China.

Among these, E2E automated driving is drawing attention as one of the functions most likely to transform user values. Tesla’s EVs currently remain at the driver-assistance level, but reportedly require driver intervention in relatively few situations, offering an experience close to full autonomy. Kuroyabu said, “Because it becomes extremely convenient and comfortable, many consumers who learn about it will not be able to go back to conventional cars.”There is also the view that widespread E2E adoption will take time, because severe accidents have occurred with automated vehicles and some users are reluctant to entrust safety and security to AI whose accident-cause analysis can be difficult. Even so, if implementation does not proceed, a country risks falling out of the global competition to collect diverse data and make AI smarter. For Japan’s automotive industry—where safety and security are major strengths as well—some argue that, in view of future global expansion and growth, “there is no time to wait to engage seriously with E2E.”

How can stable parts procurement be ensured? A mountain of issues for the SDV era

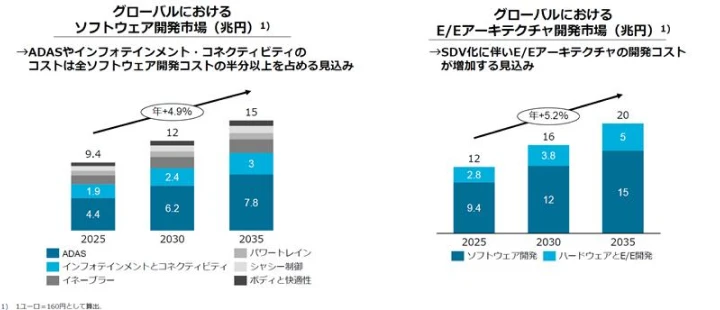

Achieving a “30% global share for SDVs” involves multiple hurdles. One is how Japan can secure and strengthen SDV-related supply chains. Estimates suggest that, as SDV adoption advances, global software development costs will rise from ¥9.4 trillion in 2025 to ¥15 trillion in 2035; and for electronic equipment (E/E architecture) such as cameras, sensors, and motors, costs will grow from ¥12 trillion to ¥20 trillion. If Japan continues to rely on foreign firms for in-vehicle software under these conditions, capital outflows will accelerate and the “digital trade deficit” will expand.

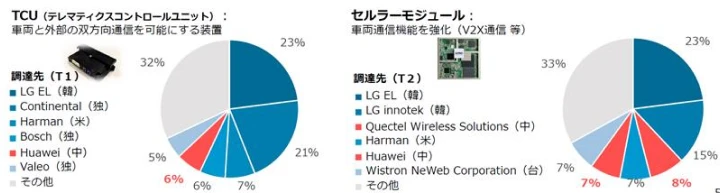

The same can be said for components and equipment indispensable for SDVs, including semiconductors and communications devices. In the design and manufacture of advanced SoCs, which form the core of systems that manage vehicles as a whole, U.S. companies such as NVIDIA and Qualcomm currently hold top shares—and those shares are reportedly increasing. In the communications-device domain, overseas players such as South Korea’s LG Electronics and the U.S.’s Harman rank high among procurement sources for key parts including TCUs (telematics control units) and cellular modules that enhance a vehicle’s communications capabilities.

From the perspective of economic security as well, Japan must nurture related industries in order to produce SDVs stably at home. In March 2024, the Advanced SoC Technology Research Association for Automobiles (ASRA) was established by OEMs such as Toyota, Honda, and Nissan together with electrical component and semiconductor manufacturers, with the aim of strengthening supply chains. The government is supporting SoC design and development required for 2030. METI is also subsidizing domestic manufacturers to ensure stable supply of next-generation power semiconductors used for electronic control.

The indispensable task of developing and securing software talent—and collaboration beyond industries

The hurdle already emerging is the need to secure and cultivate IT and wireless-communications talent that will underpin SDVs. Around the world, fierce competition for talent is unfolding among U.S. tech giants, startups, and other industries, and Japan’s automotive industry is said to face a shortage of software talent on the order of tens of thousands by 2030. Perhaps because awareness of SDVs has not yet spread sufficiently, stakeholders note that “many IT professionals do not even recognize the automotive industry as a potential employer.” This stands in contrast to the U.S. and China, where SDVs are developed in close integration with IT. As one measure to address the talent shortage, METI—working with the Society of Automotive Engineers of Japan—announced the “SDV Skills Standards” in March 2025. The standards clarify indicators such as the skills required in the software domain, and are intended as a reference tool for companies and educational institutions when developing and securing talent. METI is currently surveying how the standards have been used and is studying ways to make them easier to leverage based on the results.

Collaboration that transcends the existing automotive industry is also necessary. The PF mentioned above—outlined in the initial Mobility DX Strategy—serves this role, and it is currently made up of roughly 2,000 members from industry and academia, including participants outside the automotive sector. It has become a gathering of people who share a sense of urgency about the future of the automotive industry. Kuroyabu emphasized: “In other industries, global digitalization has drastically changed how products and services are created and what value is demanded—going so far as to force transformation of industrial structures. That wave has finally reached automobiles. Drawing on the lessons from Japan’s past, when various industries failed to fully ride global trends, the question of how the automotive industry responds is now being put to the test.”